By Michael Lewitt

Editor, Sure Money

Money Map Press

“The Walking Dead” really should just be off the air already.

Sadly, even after we’ve seen the last of this seemingly interminable show, zombies will continue to stagger across our landscape in the form of rotting corporations.

One of the arguments trotted out by corporate credit bulls is that U.S. corporations are flush with cash. That simply isn’t true. While a small number of companies –primarily tech giants – are sitting on large cash hoards, the average U.S. corporation is not cash rich and more highly leveraged than before the 2008 financial crisis. The top 1% is doing pretty well – but the other 99% are in terrible shape.

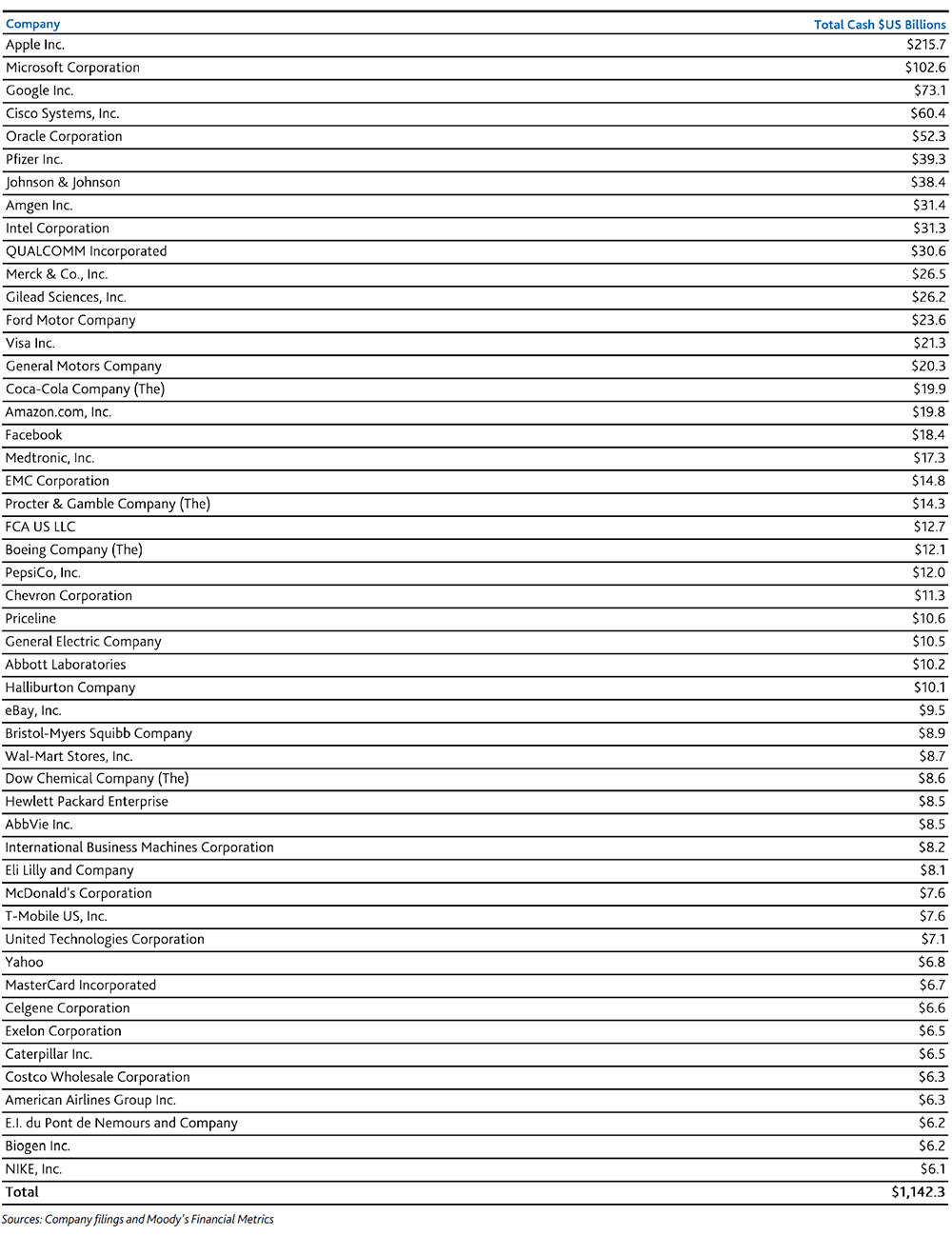

Right now, these 50 companies control about half the cash. The rest are toxic and likely to default.

Here’s what you need to know – and how to profit.

The “Dark Side” of the Balance Sheet Tells a Sobering Tale

Recently, Moody’s Investors Service and Standard & Poor’s published comprehensive reports analyzing U.S. corporate credit quality. The reports make sobering reading. While the two credit agencies’ numbers aren’t precisely the same, they are close enough and paint a troubling picture of a heavily indebted corporate sector. Relying on the excellent analytical work of Societe Generale’s Andrew Lapthorne, I warned about this situation starting in mid-2014. It wasn’t just the world’s central banks that decided to solve a debt problem with more debt. U.S. corporations have been partying like it’s 1999 when it comes to borrowing cheap money courtesy of the feckless Fed, and the result is an over-leveraged and unproductive corporate sector whose riches are narrowly shared by a small percentage of companies while the vast majority of Corporate America is being slowly suffocated by too much debt that it can never repay.

According to Moody’s, U.S. non-financial corporations rated by the firm held $1.68 trillion of cash at the end of 2015, up 1.8% from $1.65 trillion a year earlier. The top 50 holders of cash accounted for $1.14 trillion of this cash (See Figure 1). The top five companies (Apple, Microsoft, Google, Cisco and Oracle) held $504 billion of cash, or 30% of the total, up from $440 billion a year earlier and $404 billion two years earlier.

But the other side of the balance sheet told a different story.

Total corporate debt was $5.03 trillion at the end of 2015 compared to $2.62 trillion at the end of 2007. Net debt (i.e. debt net of cash) was $3.39 trillion at the end of 2015 compared with $1.88 trillion at the end of 2017. When we look deeper at the ability of corporations to service their debt, Debt/EBITDA (EBITDA measures cash flow) was 2.88x at the end of 2015 compared with 2.46x at the end of 2014 and 2.85x at the end of 2008, and speculative grade debt/EBITDA was 6.15x at the end of 2015 compared to 4.86x at the end of 2007. In layman’s terms, corporations are much more highly leveraged today than on the cusp of the financial crisis. Corporations have been able to get away with it because interest rates are much lower today than a decade ago.

Unsurprisingly, most of the cash is held by the highest rated companies. Investment grade companies hold 87% of all corporate cash ($1.4 trillion, up from $624 billion in 2007) while speculative grade companies hold only 13% ($368 billion). This tells us a few things….

- First, tracking broader conditions in our economy and society, the rich are getting richer. This is a result of monetary policy that cheapened the price of money and made it more easily available to those who need it the least and less readily available to those who need it the most.

- Second, investment grade companies are generally in good shape (other than those in the commodities industry) and probably offer a reasonably safe place to earn some modest nominal yields in a zero yield universe.

- Third, the small percentage of overall cash held by speculative grade (i.e. high yield or junk) companies is likely to prove insufficient in a serious recession or financial crisis.

As noted above, this data is consistent with the work of Societe Generale’s Andrew Lapthorne, who has warned for over two years that U.S. non-financial companies have at least 40% more net and total debt than in 2007. Goldman Sachs has also confirmed these figures. High debt levels are disguised by low interest rates but remain high nonetheless. At some point, all of this debt has to be repaid or it will default, and defaults are indeed starting to increase significantly (primarily though not exclusively in the oil patch).

Standard & Poor’s claims that total corporate debt increased by $2.8 trillion over the last five years while corporate cash rose by only $600 billion. Even more alarmingly, after backing out the top 1% of corporations, the remaining 99% saw their cash holdings fall by 6% in 2015 and held just $900 billion in cash versus $6.6 trillion of debt at the end of 2015, a cash-to-debt ratio of 15% that is even below the trough of 16% in 2008 (and down sharply from 23% in 2010). These numbers are never mentioned by the folks touting high yield bonds as a great investment in the financial media, but they are important.

The high yield market is going to see a lot more defaults as the zombie companies unable to refinance their debt end up going bust in the next 2-3 years.

———————————————————————–

[Sponsored] The world’s first “universal fuel”

Physicists have known about an unlimited source of free fuel for over 100 years. And now thanks to a stunning breakthrough in chemical engineering, we have the ability to power the entire planet for over 36,000 years. And the cost of this fuel is zero. It’s free. Click here to continue reading…

———————————————————————–

Get Out Now Before The Default Carnage Begins

This snapshot of an increasingly indebted corporate sector dovetails with other troubling trends that suggest that economic growth will continue to struggle unless the incentive structures for corporate behavior are drastically altered (which requires tax reform and fiscal policy initiatives). At the Mauldin Strategist Investment Conference in Dallas in May, David Rosenberg reiterated a point he has made for a while that capital spending is running far below what is necessary to sustain economic growth. This is consistent with research done by Lacy Hunt and Van Hoisington showing that only a small percentage of corporate borrowing is spent on productive activities such as capex and research and development . For example in 2015, corporations spent less than $100 billion of the nearly $800 billion of money they borrowed on cap ex and R&D. Instead, they devoted the majority of their expenditures – and the money borrowed to fund them – to stock buybacks, dividend increases and M&A, leaving them with less productive, more leveraged and more goodwill-laden balance sheets. In other words, they borrowed more money without improving their ability to service or repay it. Financial engineering dominates corporate activity, resulting in an over-indebted and unproductive economy that is more susceptible to shocks.

S&P raised its 2017 default rate forecast to 5.3%. Moody’s is less optimistic and raised its default rate forecast to 6% by the end of 2016. Nonetheless, the average yield on the Barclays High Yield Bond Index dropped from just over 10% in February to 7.3% on May 30. The average yield on the energy sector of the index dropped from over 17% in February to 9.82% on May 30 as well, but this is deceptive because the 70+ companies that defaulted since oil prices collapsed drop out of the index. Speaking generally (which is all you can do in evaluating broad-based investments in high yield bonds through ETFs and mutual funds and similar vehicles), a 7.3% yield on a high yield bond or 9.8% yield on an energy bond in this environment is woefully inadequate to compensate investors for the risks involved in owning them.

The jump in the default rate is in its early innings and whatever gains were enjoyed since February are likely finished as more companies default over the next 2-3 years. I continue to believe that Marty Fridson’s default forecast of $1.6 trillion of aggregate global corporate bond defaults between 2016-19 is reasonable based on a normal default cycle; if we have a recession or a financial crisis, the number will be much worse.

There are many zombie companies across a broad swathe of industries (not just commodities but retail, for example) that are only hanging on because of low interest rates and the willingness of their private equity sponsors to milk them for fees rather than restructure their debts now in order to give the businesses the debt relief and capital necessary to grow (or survive). As a result, the damage in the corporate sector is likely to be worse than in 2008. If you own high yield bonds, and especially if you own high yield ETFs and mutual funds, get out while you can. The people promoting these toxic products do not have your best interests in mind.

As Standard & Poor’s points out, “In an economy where the top 1% of companies controls over half of the cash, analyzing the U.S. corporate credit market can no longer be done on a holistic basis, or even on an investment-grade versus speculative-grade basis.” In other words, investors need to do their homework and be very selective in the bonds they buy. The ETF view of the markets doesn’t come close to telling the real story of what’s going on; it’s also a great way to lose money.

However, I do think that the fallen angel space (fallen angels are bonds that lose their investment grade ratings) looks attractive. On a risk-adjusted basis, fallen angel bonds tend to produce very attractive returns. They rarely default (except in cases of fraud or extreme changes in conditions like the current commodity collapse) and tend to be large companies with significant resources to ride out storms. Investors looking for yield should seriously consider the fallen angel space.

A simple way to play fallen angels is to buy the MV Fallen Angel ETF (NYSEARCA: ANGL).

To get full access to all Money Morning content, click here

About Money Morning: Money Morning gives you access to a team of 11 market experts with more than 250 years of combined investing experience – for free. Our experts – who have appeared on FOXBusiness, CNBC, NPR, and BloombergTV – deliver daily investing tips and stock picks, provide analysis with actions to take, and answer your biggest market questions. Our goal is to help our millions of e-newsletter subscribers and Moneymorning.com visitors become smarter, more confident investors.

Disclaimer: © 2016 Money Morning and Money Map Press. All Rights Reserved. Protected by copyright of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including the world wide web), of content from this webpage, in whole or in part, is strictly prohibited without the express written permission of Money Morning. 16 W. Madison St. Baltimore, MD, 21201.

One thing stands out to me from this list. There are no commodity companies. That is what Jim Rogers would call an opportunity.

Commodities have been beaten down,their cash positions are low but they are still producing and in a cash flow situation.

Check out ENZL ETF fund. This country exports 40% of the world’s need for dairy products. See their chart.

If you believe the collapse is coming, these top 50 companies are in jeopardy. But the world will continue to need milk and dairy products. Jim did not make his fortune following the crowd. He looked for opportunity.